![]()

Call Now: (+61) 416-195-006

ACCT 6004 GROUP CASE STUDY ASSIGNMENT

Activity 4: Activity Based Costing at J&B Sports

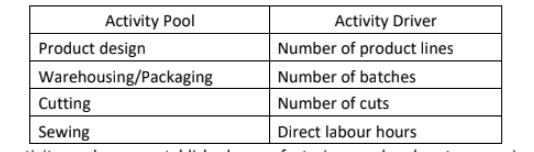

The new internal accountant at J&B Sports is concerned about the current method of allocating overhead to production, using a volume-based allocation base (direct labour cost) and one plant-wide overhead rate. She decided to undertake an activity analysis across the manufacturing processes of the company and to identify the relevant cost drivers of these.She determined that J&B Sports had the following four activity pools and associated activity drivers:

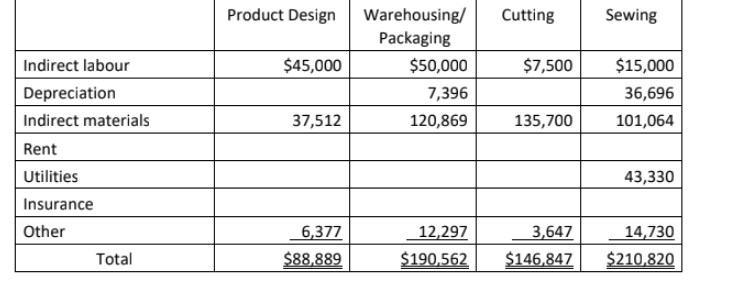

Once the activity pools were established, manufacturing overhead costs are assigned to

these:

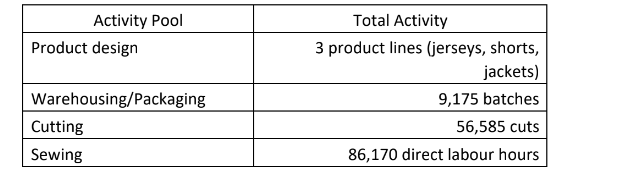

Data was also collected on the activity drivers for each activity pool:

Chris Desmond, J&B Sports’ operations manager, recently received a sales brochure for a new electric cutting tool. Based on the tool’s specifications, Chris believes that J&B Sports could increase the batch size on jersey production to 50 jerseys, up from the current 35 jerseys.

While the cutting tool would be used on shorts and jackets as well, other production factors prevent increasing the batch sizes for these products. The new tool would increase annual operating costs by $15,090. Before deciding whether to purchase the cutting tool, Chris wants to know how the new tool will affect the cost of producing the company’s three main products.

Required:

b. Classify each activity using the ABC cost hierarchy categories.

Expert's Answer

Chat with our Experts

Want to contact us directly? No Problem. We are always here for you